Venture Capital Fund & Angel Fund Under SEBI (Alternate Investment Fund) Regulations 2012 Explained

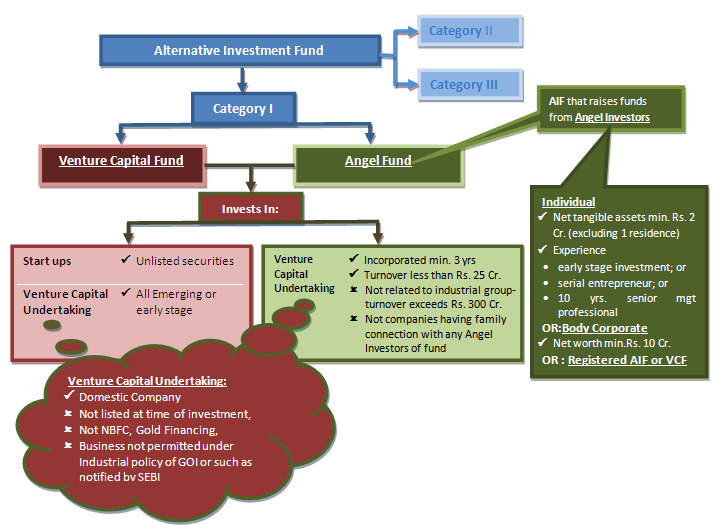

As per SEBI (Alternative Investment Funds) Regulations, 2012, 3 broad categories of funds have been classified to be registered under said regulations namely Category I, II, and III. Under Category I, there are further classification namely:

(a) Venture Capital Fund

(b) SME Fund

(c) Social Venture Fund

(d) Angel Fund

Though the purpose of AF and VCF both are to promote Venture Capital Undertakings,there are several difference between the both with respect to category of Investors, Investee Company, Limits of Investments etc. which are discussed in detail hereunder.

Basic Structure and Definitions

So far as basic structure of Angel Funds in comparison to that of Venture Capital Funds are concerned, the prime difference lies in the Investor and Investee criteria or standards defining them.

Investors

Firstly w.r.t. to Investors, in case of VCF, any person/investor can pool in fund with minimum investment amount of Rs. 1 Cr. Alternatively in case of Angel Funds, only Angel investors can pool in fund. The Regulations have further provided that which entities can be termed as Angel Investors which broadly to include individuals having net tangible asset value of Rs. 2 Cr. or a body corporate with net worth of Rs. 10 Cr.

Investee Companies

Further w.r.t. to Investee Company, though both VCF or Angel Fund are required to invest in Venture Capital Undertakings(VCU)(as described hereunder), though herein too in case of Angel Fund, the VCU must be such which are not more than 3 years old and must have maximum turnover of Rs. 25 Cr. etc. though a VCF can invest in any VCU irrespective to years or networth.

The same is detailed herein below:

Comments